When the pandemic hit in 2020, many experts thought the housing market would crash. They feared job loss and economic uncertainty would lead to a wave of foreclosures similar to when the housing bubble burst over a decade ago. Thankfully, the forbearance program changed that. It provided much-needed relief for homeowners so a foreclosure crisis wouldn’t happen again. Here’s why forbearance worked. Forbearance enabled nearly five million homeowners to get back on their feet in a time when having the security and protection of a home was more important than ever. Those in need were able to work with their banks and lenders to stay in their homes rather than go into foreclosure. Marina Walsh, Vice President of Industry Analysis at the Mortgage Bankers Association (MBA), notes:

“Most borrowers exiting forbearance are moving into either a loan modification, payment deferral, or a combination of the two workout options.”

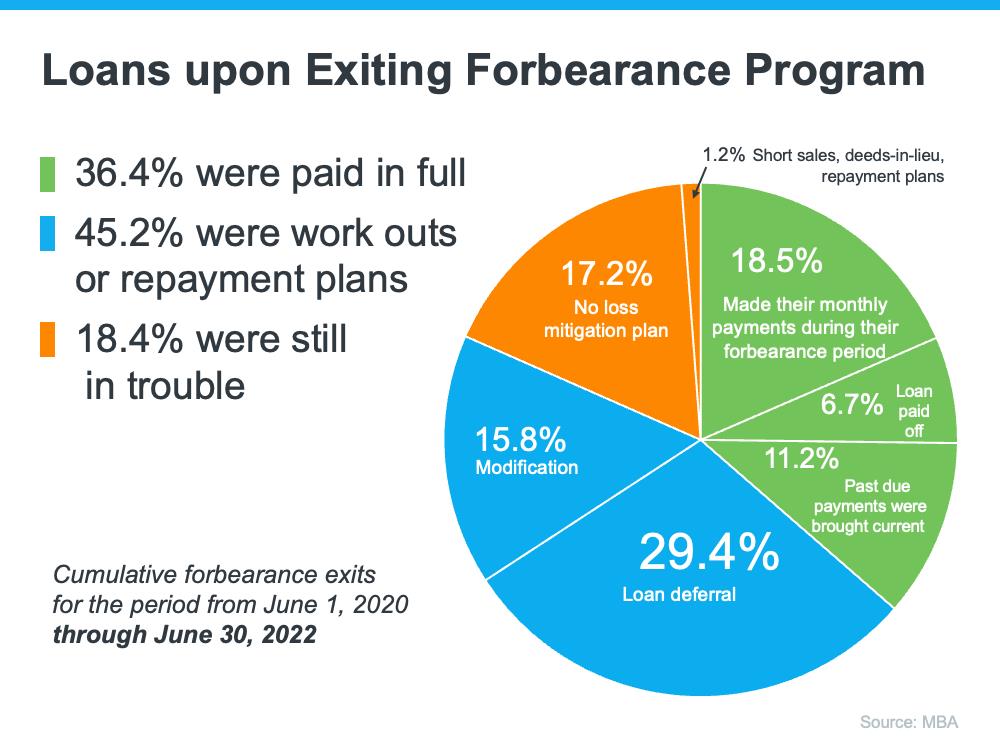

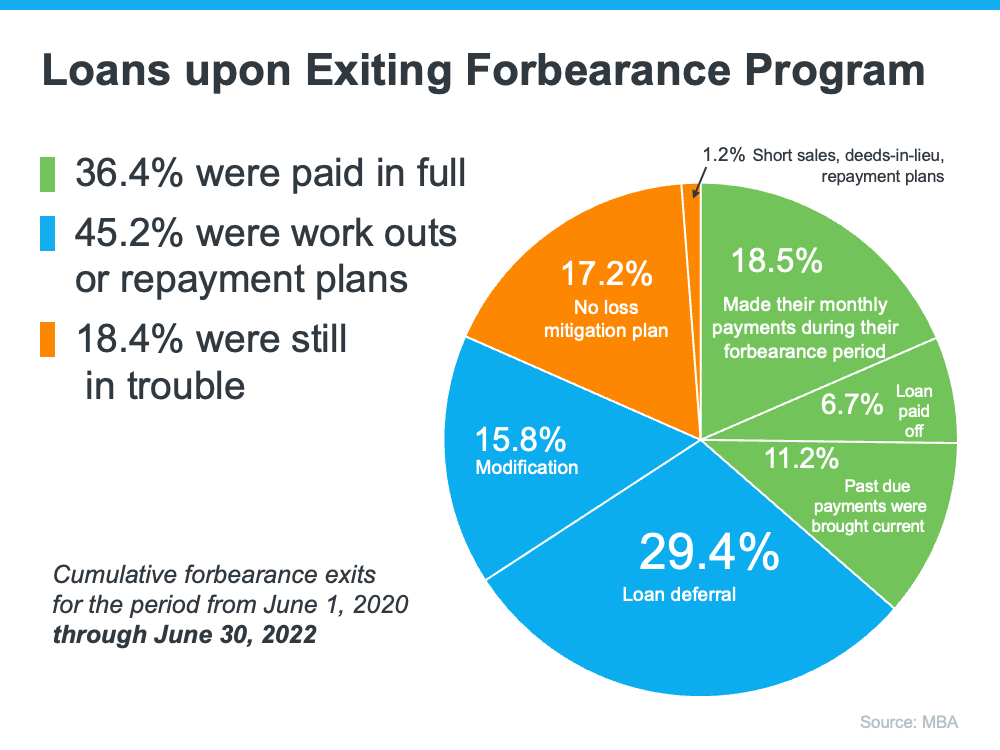

As the graph below shows, with modification, deferral, and workout options in place, four out of every five homeowners that were in forbearance either exited paid in full or are exited with a repayment plan. They were able to stay in their homes!

What does this mean for the housing market?

Since so many people were able to stay in their homes and work out alternative options, there hasn’t a wave of foreclosures coming to the market. And while rising slightly since the foreclosure moratorium was lifted, foreclosures today are still nowhere near the levels seen in the previous housing crisis. Forbearance wasn’t the only game changer, either. Lending standards have improved significantly since the housing bubble burst, and that’s another factor in keeping foreclosure filings low. Today’s borrowers are much more qualified to pay their home loans. And while the majority of homeowners are exiting, or have exited, the forbearance program with a plan, for those who still need to make a change due to financial hardship or other challenges, today’s record-level of equity is giving them the opportunity to sell their houses and avoid foreclosure altogether. Homeowners have options they just didn’t have in the housing crisis when so many people owed more on their mortgages than their homes were worth. Thanks to their equity and the current undersupply of homes on the market, homeowners can sell their houses, make a move, and not have to go through the foreclosure process that led to the housing market crash in 2008. Thomas LaSalvia, Chief Economist with Moody’s Analytics, states:

“There’s some excess savings out there, over 2 trillion worth. . . . There are people that have ownership of those homes right now, that even in a downturn, they’d still likely be able to pay that mortgage and won’t have to hand over keys. And there won’t be a lot of those distressed sales that happened in the 2008 crisis.”

What If You Need a Forbearance Program Now?

Forbearance programs were very effective during the economic stress of COVID. Yet, current economic conditions have stressed many homeowners’ budgets generating concern about being able to make the mortgage payment. If you need help now, there are still options but some of the COVD-era forbearance options may be ending soon. What is available today?

1. Homeowner Assistance Fund (HAF program)

The American Rescue Plan Act of 2021 created the Homeowner Assistance Fund (HAF) to provide federal assistance to people struggling with their housing payments.

Eligible homeowners who receive money from the fund can use it to catch up on past-due mortgage payments. They can also pay other housing-related bills. These include homeowners insurance, property taxes, utilities, and even home repairs.

To be eligible for HAF funds, homeowners can’t earn more than 100% of the U.S. median income or 150% of their area’s median income, whichever is higher.

The Act set aside $10 billion for all 50 states, the District of Columbia, and other U.S. territories, such as Puerto Rico, for housing assistance. (The American Rescue Plan also set up a separate fund for rental assistance.)

The money for the HAF program comes from the U.S. Department of the Treasury. However, states distribute funding on their own terms and many state programs have ended.

2. Refinance to lower your payments

For some homeowners, refinancing into a new mortgage can offer relief by reducing their monthly payments.

Currently, with rising mortgage interest rates, it is difficult to get a new loan with a lower rate. But even if you can’t lower your mortgage rate, extending your loan’s term could reduce your monthly payments. While you will owe more interest in the long run by extending your loan’s term, the lower monthly payment may be the relief your budget needs.

Refinancing with low equity

Home values skyrocketed in many areas over the past few years, leaving less than 2% of all mortgaged homes underwater. Even homeowners who made a very small down payment or refinanced recently could still have enough equity to qualify for a refinance.

And, you might not need great credit or perfect finances to qualify for a refinance. Select programs, like the government-backed Streamline Refinance, may be able to help borrowers refinance their mortgage with little, no, or even negative home equity.

Refinancing after forbearance

Already been in a forbearance program? In the past, it could be difficult to refinance your home loan after being in a forbearance plan. But those rules have loosened up. This is due to the unprecedented spike in mortgage forbearance during the COVID pandemic.

Now, it’s possible for many homeowners to refinance in as little as three months after ending their forbearance plans. Application guidelines can vary by loan program and mortgage lender. So talk to a loan officer or mortgage broker to learn whether you meet the eligibility requirements.

3. Other mortgage assistance programs

The well-known CARES Act, which Congress passed in 2020 as a part of the federal COVID assistance efforts, also included mortgage assistance programs. However, the program ended earlier this year including the mortgage assistance programs. But if you need help, check with your loan servicer about these mortgage relief programs:

Mortgage forbearance

Loan forbearance temporarily pauses your monthly mortgage payments while you go through financial hardship. The debt isn’t forgiven — you’ll have to make up the missed payments after forbearance ends — but this payment suspension can provide some breathing room while you get back on your feet financially.

Your current forbearance options depend on what type of mortgage loan you have and whether you’ve used a forbearance plan previously.

- Conventional loans (backed by Fannie Mae or Freddie Mac): If you have not yet requested forbearance, you can still do so. There is no deadline for requesting initial loan forbearance on conventional mortgages.

- Government-backed loans (FHA, VA, or USDA): Homeowners with loans backed by FHA, VA, and USDA can no longer request forbearance. This was an option while the COVID-19 National Emergency was in effect but the emergency declaration expired in January 2023. It would still be advisable to contact your mortgage holder to see what options are available.

Once your loan forbearance period expires, you’ll have a few options for how to exit forbearance and repay your missed loan payments.

Your loan servicer cannot ask you to repay everything in a lump sum right after exiting forbearance. You’ll likely pay the missed amount in installments along with your regular mortgage payments or defer repayment until you sell the home or refinance.

Loan modification

For homeowners who need to exit forbearance but don’t qualify for a refinance, another option could be a loan modification.

Modification is for homeowners who have had a permanent, rather than a temporary, change in their financial circumstances. This involves your loan servicer agreeing to lower your rate or extend your loan term to make the mortgage payments more affordable.

Homeowners with FHA, VA, and USDA loans might still be able to take advantage of Biden’s 2021 mortgage stimulus program, which lowers payments by as much as 25% via a loan modification. However, at this point in 2023, availability is very limited for vulnerable populations.

Loan modification is typically a last resort for homeowners who can’t refinance or take advantage of other mortgage relief programs.

4. State housing counseling agencies

A HUD-approved housing counselor in your state may know about some mortgage assistance programs that are available in your community.

Counselors know about local government and non-profit agencies that can offer mortgage relief. In addition, HUD-approved housing agencies usually offer foreclosure prevention counseling for free.

5. Mortgage relief options from Fannie Mae and Freddie Mac

Homeowners with conforming loans — those backed by Fannie Mae or Freddie Mac — have specific options for mortgage relief.

If you’re experiencing a temporary hardship, it’s not too late to ask about forbearance. There’s currently no deadline to make an initial forbearance request with your loan servicer.

In addition, Fannie and Freddie offer expanded refi programs. These can make it easier and cheaper to lower your interest rate and mortgage payment.

Fannie Mae’s RefiNow and Freddie Mac’s Refi Possible are designed for low- to moderate-income homeowners. You might qualify if you make an average or below-average income for your area.

These refinance programs have unique benefits that can offer financial relief to homeowners, including:

- Lower mortgage rate and monthly payment

- Reduced closing costs with no appraisal fee

- Easier debt-to-income qualification

These new loan options can offer big savings for homeowners who might not otherwise qualify to refinance.

6. Contact your lender about mortgage relief

If you’re worried about paying your mortgage, reach out to your lender directly for mortgage relief, regardless of the loan type or any available government assistance.

Don’t hesitate to call even before you miss a payment. Taking early action can likely provide you with more mortgage relief options. If you’ve already missed a payment and request forbearance, be aware that the delinquency might reflect on your credit report, lingering until you bring the loan current again.

When reaching out to your lender, make sure you have the following at hand:

- Your current income estimate and anticipated future income if you expect changes

- A summary of your current monthly expenditures

- The latest mortgage statement

- Any documents that explain changes in your financial situation

Finally, be very cautious of third parties that offer mortgage assistance to you (often for a fee). Rather, seek help directly from your lender instead. If you need guidance on speaking with your lender, you can find a HUD-approved financial counselor on the HUD website. They provide assistance at no cost and can equip you to have a more effective conversation with your lender.

Bottom Line

Forbearance programs have been game changer for homeowners in need. It’s one of the big reasons why we haven’t and won’t see a wave of foreclosures coming to the market. And there are still options should you need help today. If you have questions, get in touch and let’s talk – your biggest asset is your home so let’s work to protect it.

Sources include: Mortgage Assistance & Relief Programs | 2023 (themortgagereports.com)

{kind=link}